Brokers Digest: Local Equities - Power & Utilities Sector, RHB Bank Bhd, Eastern & Oriental Bhd, DRB-Hicom Bhd

This article first appeared in Capital, The Edge Malaysia Weekly on October 23, 2023 - October 29, 2023

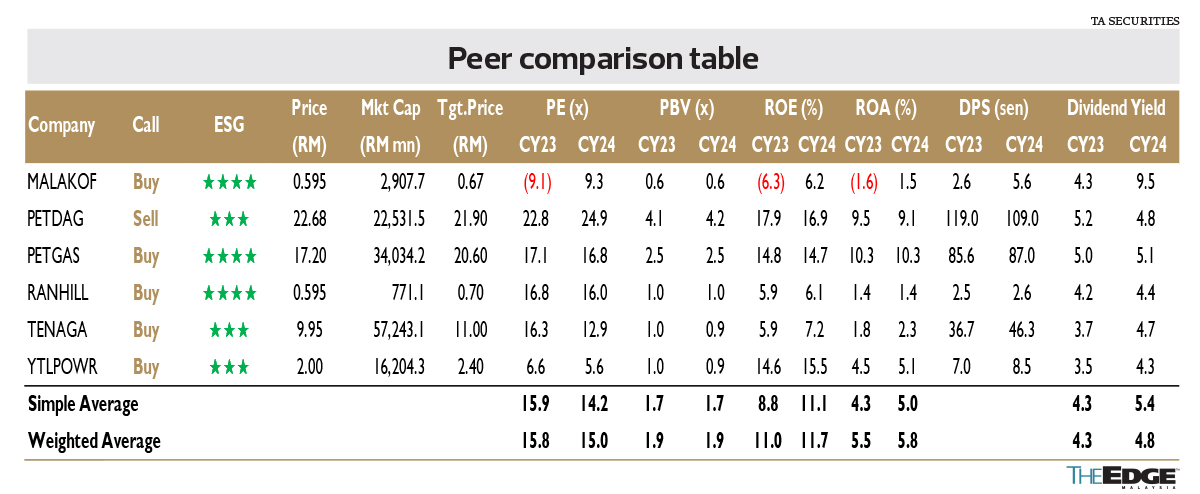

POWER & UTILITIES SECTOR

OVERWEIGHT

TA SECURITIES (OCT 17): The measures for Budget 2024 are mildly positive for the power and utilities (P&U) sector. There were no major surprises. In fact, we are disappointed that the government has yet to roll out the mechanism for the renewable energy (RE) exchange hub. Although the ban on cross-border exports of RE was lifted in May, we understand that Malaysia is currently not exporting any RE to Singapore pending the finalisation of the RE exchange hub. Note that Malaysia is short on time as the deadline to submit a non-binding expression of interest proposal to the Energy Market Authority (EMA) of Singapore for the second request for proposal (RFP2) to appoint licensed electricity importers will be in two months, on Dec 29.

The expansion of targeted electricity subsidy (by removing the subsidy for the top 10% users) does not come as a surprise. Additionally, there is an increase in service tax from 6% to 8% for monthly consumption above 600kWh. We expect both measures to lead to demand reduction for residential consumers. However, considering that Tenaga Nasional Bhd (“buy”, target price: RM11) is largely shielded from demand risk as the group can f the revenue shortfall, we do not expect material impact on the group’s earnings. Meanwhile, the increase in selling price for diesel will lead to demand destruction and will adversely impact Petronas Dagangan Bhd (“sell”, target price: RM21.90).

The construction of an electricity transmission line in southern Sabah, which is situated on the east coast, will allow more electricity transmission from the west coast to southern Sabah. Ranhill Utilities Bhd (“buy”, target price: 70 sen) is the prime beneficiary as the group currently has two power plants with a total 380MW power generation capacity on the west coast of Sabah. On the allocation of RM1.1 billion to solve water supply issues in Kelantan, Sabah and Labuan, some of the potential beneficiaries are Engtex Group Bhd and YLI Holdings Bhd (both not rated), which manufacture pipes for waterworks.

We maintain our “overweight” call on the P&U sector as we believe companies in the sector will gain exciting earnings growth opportunities as they embark on Malaysia’s energy transition aspirations. A further upside catalyst for the sector will be from the finalisation of Malaysia’s RE exchange hub, hopefully by the end of this year.

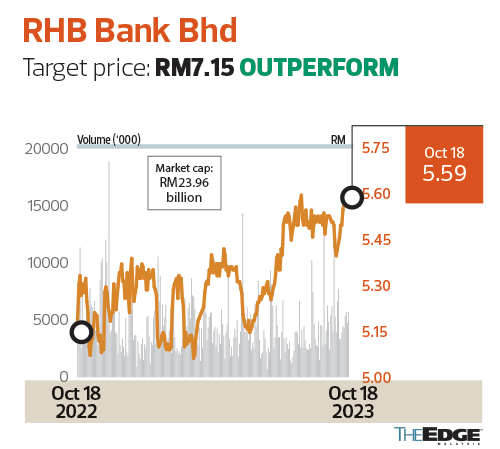

RHB Bank Bhd

Target price: RM7.15 OUTPERFORM

KENANGA RESEARCH (OCT 17): For FY23, the group anticipates loan growth of 4%-5%, which is in line with our broader industry target. The group is still seeing sustained demand from its community and small and medium enterprise (SME) banking segments.

Margins could remain under threat. RHB Bank’s 1HFY23 net interest margin (NIM) was marked at 1.85% (FY22: 2.24%) as it was not spared the intense deposit competition spurred by rising overnight policy rate (OPR) expectations in December. Despite two consecutive quarters of margin erosion, the group may continue to see readings coming off as product rates could remain competitive in spite of peers consciously easing down their product rates.

With regards to its upcoming digital bank venture with Axiata-Boost, the group is optimistic that it can pass Bank Negara Malaysia’s operational readiness review during the quarter. The group is also hopeful to debut its maiden deposit product earliest by 4QFY23, with financing offerings later on. That said, its target markets will lean towards microfinancing as mandated by the central bank for the digital bank licensees’ foundational stage.

Eastern & Oriental Bhd

Target price: 88 sen BUY

RHB INVESTMENT BANK (OCT 16): The upcoming relaxation of Malaysia My Second Home (MM2H) requirements is expected to benefit areas that are typically favourite spots for foreign property buyers. These include Penang island, Kuala Lumpur’s KLCC and Mont’Kiara areas, and Iskandar Malaysia in Johor. Eastern & Oriental (E&O), as a proxy for a Penang island property play, is set to benefit from this new measure, which was announced recently. In the past, about 20% of E&O’s buyers were foreigners.

The extension of the light rail transit (LRT) line to Tanjung Bungah will benefit Andaman Island. The Bayan Lepas LRT line, originally planned to connect Penang International Airport to Komtar, will now be extended all the way to Tanjung Bungah. As the final Tanjung Bungah station is only about 2.5km from Andaman Island (via the Gurney Bridge which is currently under construction), we think this new transport infrastructure will likely spur investment opportunities for E&O’s projects going forward.

E&O’s fundamentals and earnings prospects have improved, especially after new major shareholder Datuk Tee Eng Ho took over the company in 2021. Our target price of 88 sen is in line with the recent sector rerating.

DRB-Hicom Bhd

Target price: RM2.10 OUTPERFORM

PUBLIC INVEST RESEARCH (OCT 17): We visited DRB-Hicom’s Proton manufacturing plant in Tanjung Malim and remain positive about its growth strategy toward achieving a sales target of 310,000/500,000 units by 2030/2035, of which 50% are to be new energy vehicles (NEV) and for the export market.

The ambitious target will be driven by its partnership with Geely and the development of the Automotive Hi-Tech Valley (AHTV) project, which will transform Tanjung Malim into a global automotive hub for NEV. Geely owns and manages a number of brands including Geely Auto, Lynk & Co, ZEEKR, Geometry, Volvo Cars, Polestar, LEVC, Radar Lotus, Smart and Livian.

About 50 vendors are expected to move into the new facilities in AHTV in the next few years. The AHTV is expected to attract RM32 billion worth of investments over the next 10 years and expand the capability of local vendors in specialising in high technology manufacturing.

However, we keep our estimates unchanged for now as we are not expecting any near-term impact arising from this project. We continue to like DRB’s growth prospects and retain our “outperform” call with an unchanged target price of RM2.10.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

| DRBHCOM | 1.380 |

| E&O-LC | 1.090 |

| ENGTEX | 1.000 |

| KENANGA | 1.140 |

| KLCC | 7.500 |

| PETDAG | 21.460 |

| RANHILL | 1.390 |

| RHBBANK | 5.500 |

| TENAGA | 12.400 |

| UTILITIES | 1743.380 |

| YLI | 0.520 |

Comments