A less risky route to buying China’s eventual recovery

This article first appeared in The Edge Malaysia Weekly on March 25, 2024 - March 31, 2024

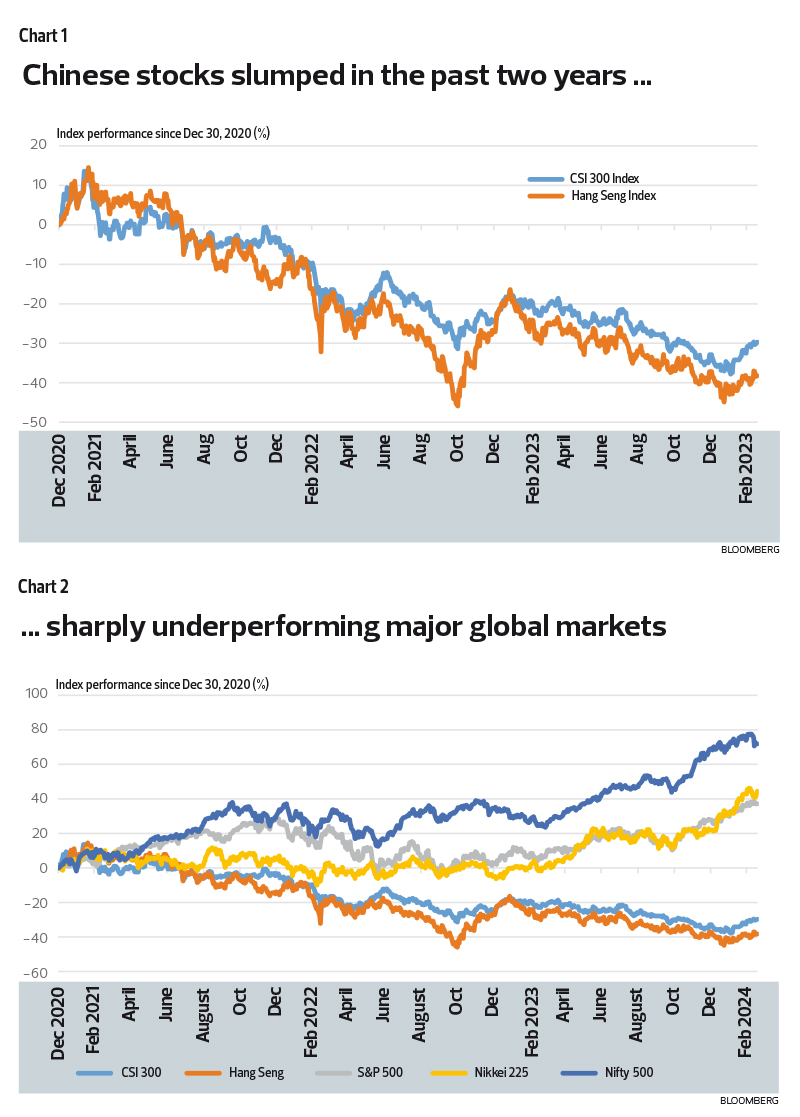

Have Chinese stocks bottomed out and are there now opportunities to be had? The Chinese stock markets in Shanghai and Shenzhen have slumped over the past two years while stocks listed on the Hong Kong bourse have fared even worse, on heavy foreign selling and capital outflow.

The brief fillip in anticipation of the post-pandemic reopening, in 4Q2022, has very quickly fizzled out. And although the China market benchmark CSI 300 Index recovered some lost ground in the past few weeks — on the back of domestic and state-backed fund buying, coupled with short-selling restrictions and a crackdown on high-speed trading — it remains below pre-pandemic levels. There are a myriad of reasons for this underperformance, a stark contrast to major global markets.

Plenty has been written about China’s current economic slowdown, weighed down by its troubled property sector, sluggish domestic consumption as well as negative export growth on the back of weaker global demand. On top of this, there is the ever-growing rift with the US-led Western world and escalating trade restrictions — on both imports and exports — related to high-tech sectors.

China’s economic growth will slow — and may even stay sluggish for some time. For one, it is now the second-largest economy in the world; therefore, it is not realistic that the economy would continue to growth at previously high rates. China is targeting GDP growth of around 5% this year, the same as for 2023, which is a sharp moderation from previous growth rates (average of 9% between 1999 and 2019).

It is also an economy in transition — from one that is driven primarily by exports and infrastructure to one that is more reliant on domestic consumption and sector-focused investments. As we know, protectionism is rising around the world and globalisation is in reverse. Global trade as a percentage of GDP has peaked and may continue to fall on the back of geopolitics and the resurgence of large-scale industrial policies in developed countries such as the US. Investments, especially related to its troubled property sector, are slowing too (more on this later).

Meanwhile, household consumption has yet to pick up the slack. Consumer confidence is low, shaken by the property slump — given its high home ownership and the fact that property has been the preferred investment asset in the country. The lack of a social safety net also means that the savings rate remains comparatively high.

Thus, many remain sceptical about whether the above-mentioned stock market support measures alone can sustain the share price recovery. Foreign investors are also disappointed that the Chinese government has consistently ruled out massive stimulus to boost the economy, favouring targeted support for the property sector and ensuring the financial system has ample liquidity. While massive stimulus may provide a short-term boost, it will not address the country’s structural economic problems. There is clearly less necessity for China to apply a “steroid” policy to gain short-term popularity to win elections. In other words, China is focused on “quality growth” rather than simply “growth for the sake of growth”.

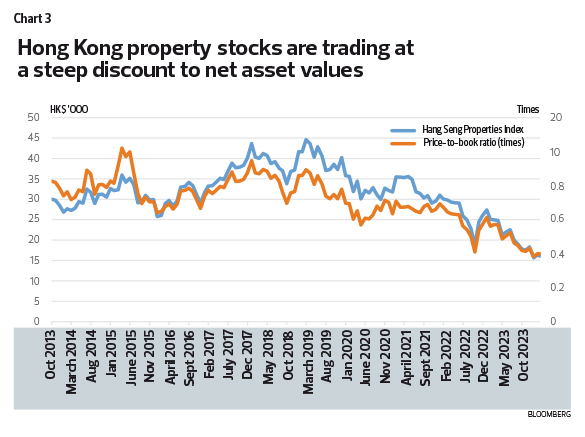

As geopolitical tensions and uncertainties grow, foreign monies — foreign direct investments (FDI) and portfolio funds — are de-risking, diversifying investments into regional countries such as Asean, India and Japan. In contrast to the slump in Chinese stocks, India and Japan’s stock markets have soared. The Nikkei 225 recently breached its previous all-time-high record achieved in 1989, before its asset bubble burst (see Charts 1 and 2).

Analysts are almost universally bearish on Chinese stocks right now, and that itself is probably a signal to be a contrarian. But the short answer as to whether stocks have hit bottom is: We do not know. And we doubt any of the “China experts” know for sure either. So, let us take a page from the Warren Buffett investing handbook — forget about obsessing over market timing, a near-impossible task, and focus on the fundamentals.

Yes, there are downside risks. But the potential upside gains, we think, are far greater from hereon, considering prevailing cheap valuations, relative to other major markets such as the US. In particular, Hong Kong property stocks, we think, are attractive risk-reward propositions at current prices. One just needs to be patient and have the holding power.

Remember, do not borrow to invest! Especially not when you do not know when the turnaround will materialise. Stock markets driven by momentum will often overshoot fundamentals, on both the upside and downside. And, right now, the momentum is towards the downside.

One strategy would be to pace your investments, accumulate slowly and learn as you go along. We believe that at some point, over the next couple of years, there will be a big move up. And you don’t want to not be part of the game then.

Hong Kong property stocks, at less than 0.4 times P/B, are good risk-reward propositions

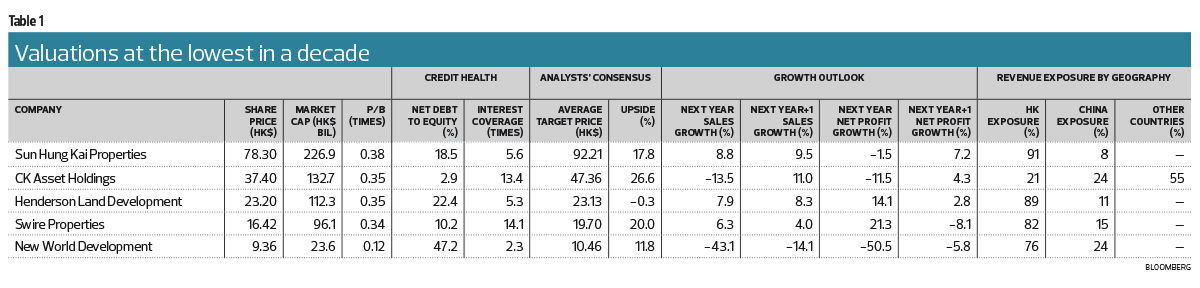

Hong Kong property stock prices and valuations have collapsed since the pandemic — the Hang Seng Properties Index is currently near its Global Financial Crisis (GFC) lows — beset by woes in the Hong Kong and China property markets as well as a weaker economic outlook (see Chart 3).

Yes, it will take time for both property markets to recover, but we have no doubt that they will. And property developers such as Sun Hung Kai Properties (the largest developer in Hong Kong) and Swire Properties have fairly strong balance sheets to ride out the demand and earnings downturn. Notably, the stocks are trading at the lowest price-to-book values in at least a decade, at only 0.38 times and 0.34 times net asset value respectively (see Table 1).

The last China property upcycle was driven, in large part, by speculation. The government’s clampdown on excessive developer debts in 2020 burst that bubble, and sent tens of its domestic developers, including some of the largest in the country such as Country Garden and Evergrande, into financial distress — and leaving millions of uncompleted but pre-sold homes. That shook home buyer confidence and demand contracted sharply, feeding the vicious cycle of falling sales and asset values held by property developers as collateral for financing.

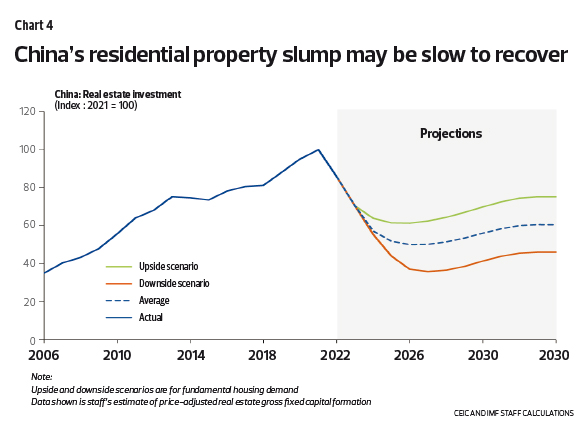

Property sales have continued to slide, even after the central bank lowered mortgage rates. Buyer confidence remains low on fears that the sector’s financial troubles are still far from being resolved and home prices — whose decline has been modest thus far — could fall further. Rebuilding buyer confidence will take time (see Chart 4).

The residential property market in Hong Kong is also in a slump, for different reasons. As we noted, property developers are in comparatively good financial health. Demand and, particularly, primary sales contracted steeply in 2022/23, when the mortgage rate soared with the US Federal Reserve’s aggressive interest rate hikes.

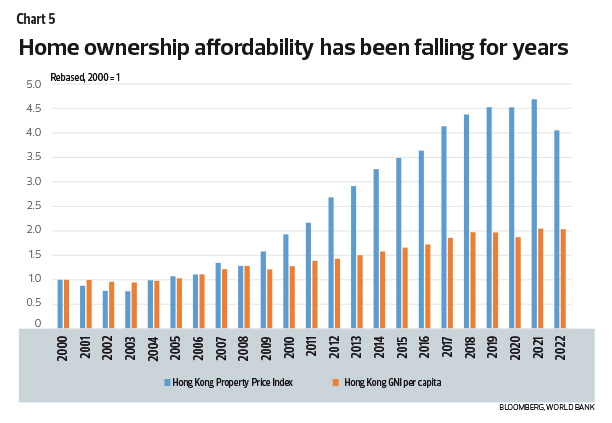

Sharply higher mortgage payments worsened home ownership affordability, which had already been falling for years since the GFC — house prices appreciated at a far faster pace than income growth (see Chart 5). The post-pandemic economic rebound also turned out to be weaker than expected.

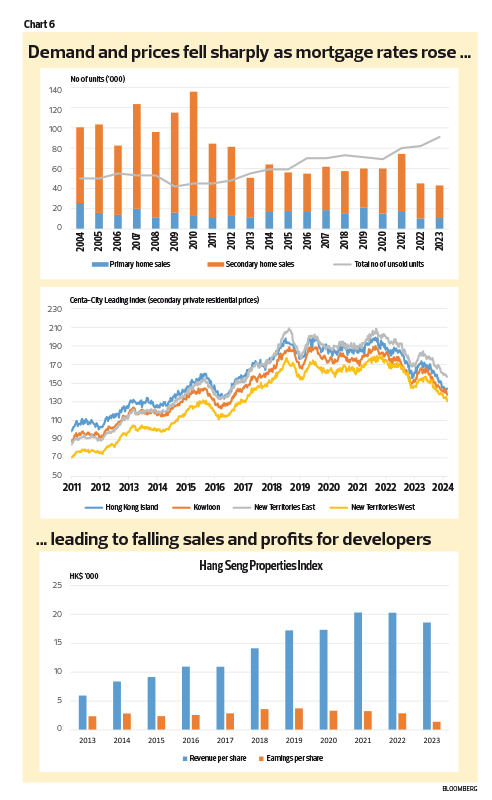

The number of unsold property units rose, and property prices fell. Despite a gradual relaxation of previous measures to curb speculation through 2022/23, demand stayed weak and property prices continued to decline. As a result, most property developers suffered a revenue and profit drop (see Chart 6). And their share prices and valuations collapsed on the back of a poor outlook (see Chart 3).

Positively, we suspect that the worst may be over for Hong Kong’s property market. Case in point: The sector reported the best weekend of sales in a year — immediately after the government’s scrapping of all its remaining decade-old cooling measures (including for foreign buyers) in the latest Budget 2024, in a bid to revive the flagging property market.

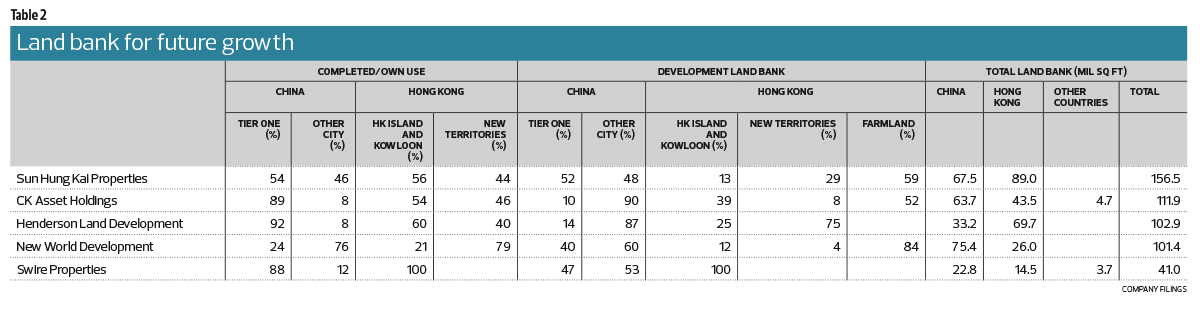

The mortgage rate is likely to have peaked, with the Fed expected to start cutting interest rates later this year. Coupled with the property price correction, affordability should gradually improve and help put a floor to demand. Over the longer term, population growth — including immigration — is expected to stay positive (at least for the next two decades) while household size is on a downtrend. The Chinese government’s economic development plan for the Greater Bay Area should also boost property demand, particularly in the Northern Metropolis area, where many of the property developers have land banks (see Table 2).

In summary, we cannot be certain whether the Hong Kong property market — and hence property stock prices — has bottomed out. It will take time for the market to work through existing unsold inventory. In addition, almost all of the major Hong Kong property developers have some exposure in the mainland property market, where a worsening outlook has further hurt overall investor sentiment. China’s property market turnaround may take longer. At prevailing low valuations, however, further downside from hereon must be limited compared to the potential upside gains.

Picking the bottom is always difficult and often not very rewarding for many investors — the wait is long and demands too much patience. So, it is really for very long-term investors — much like investing in land, not the developers — who are willing to sit and simply wait. And, for many of these investors, they have made the real big money!

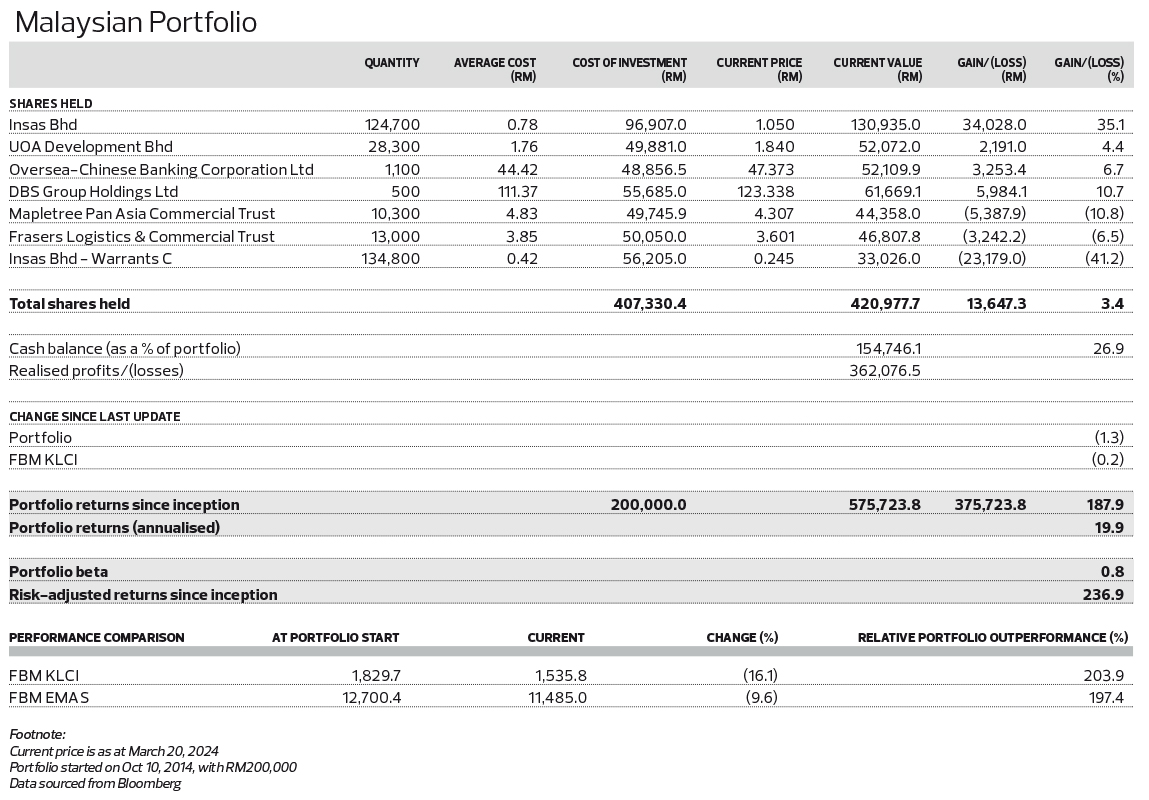

Stocks in the Malaysian Portfolio fell 1.3% for the week ended March 20. The biggest losers were Insas-WC (-12.5%) and Mapletree Pan Asia Commercial Trust (-6.6%). On the other hand, DBS Group Holdings (+3.3%), Oversea-Chinese Banking Corporation (+1.7%) and UOA Development (+1.1%) ended higher for the week. Total portfolio returns now stand at 187.9% since inception. This portfolio is outperforming the benchmark FBM KLCI, which is down 16.1%, by a long, long way.

Disclaimer: This is a personal portfolio for information purposes only and does not constitute a recommendation or solicitation or expression of views to influence readers to buy/sell stocks. Our shareholders, directors and employees may have positions in or may be materially interested in any of the stocks. We may also have or have had dealings with or may provide or have provided content services to the companies mentioned in the reports.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

Comments