MyEG's short-selling suspended after gapping down on news all immigration services to revert back to govt by 2025; Iris sees jump in interest

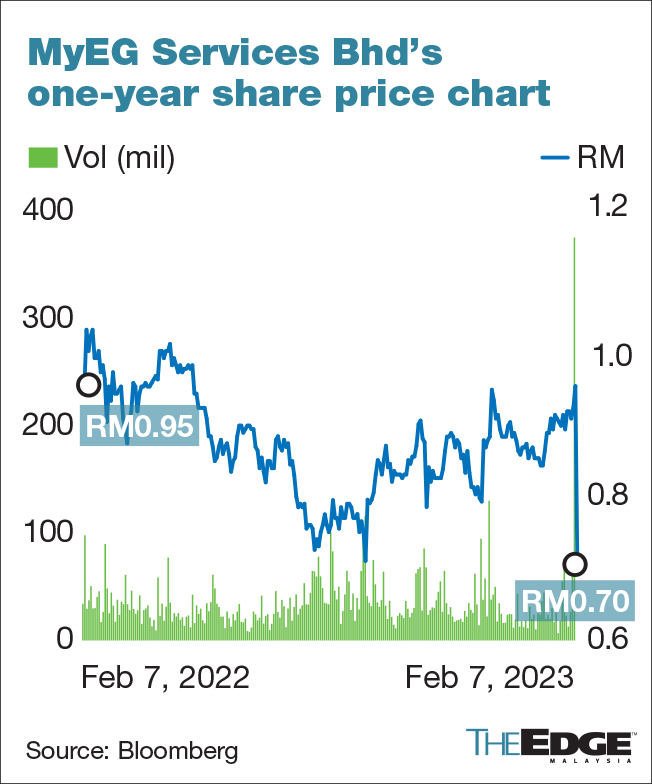

KUALA LUMPUR (Feb 7): MyEG Services Bhd gapped down on market opening to 65.5 sen on Tuesday (Feb 7), down 30 sen or 31.41% from last Friday's close, following news reports that all immigration services and processes will revert back to the Immigration Department by 2025, including those being managed by third parties such as MyEG.

This is because of the implementation of the national integrated immigration system or NIISe, which will converge all immigration transactions, including passport renewals, visa applications, applications and renewals of permits for foreign workers, according to the New Straits Times on Monday.

Immigration director general Datuk Seri Khairul Dzaimee Daud was quoted as saying that the Home Ministry had set aside RM900 million for the roll-out of NIISe in two years, and that the new system is expected to be a "game changer" that would improve the department's efficiency and customer experience.

NIISe, which is currently developed by Iris Corp Bhd, will replace the current Malaysian Immigration System (myIMMS) that the department has been using for about 13 years.

Short-selling suspended

At the time of writing, MyEG had pared some losses to trade at 70 sen a share.

Shortly after market opening, Bursa suspended short-selling of the stock for the rest of the day under proprietary day trading (PDT) and intraday short selling (IDSS), after the stock dropped more than 15 sen or 15% from its reference price.

“Short-selling under PDT and IDSS will only be activated the following trading day, on Wednesday, at 8.30am,” the stock exchange regulator said in a filing.

Iris Corp, on the other hand, gapped up to 13.5 sen from 12.5 sen at last Friday's close, and jumped to as high as 19 sen. At the time of writing, it was trading at 16.5 sen, up 32%, with 131.95 million shares traded. It was the second most active stock in the morning after MyEG, which saw over 400 million shares done.

Affin Hwang Investment Bank said in a note on Tuesday that the news is negative for investor sentiment, and may affect MyEG's long-term earnings trajectory. It downgraded the stock to "hold" from "buy", and cut its 12-month target price for the stock to 93 sen from RM1.23.

It estimated that immigration-related services contribute to 40-50% of MyEG's revenue.

"These immigration-related services include the renewal of foreign workers’ work permits (10-15% of total revenue) and other ancillary and commercial services, such as renewal of foreign workers’ insurance and foreign worker job matching (30-35%). In May 2020, the government extended MyEG’s contract for the provision of online renewal of foreign workers’ work permits for three years to May 2023. The loss of services, if reverted to the Immigration Department as planned, may impair MyEG’s long-term revenue (2025 and beyond) by about 20%."

'There could be changes to deployment of NIISe project'

Affin Hwang IB, however, believes that the full deployment of NIISe by 2025 is "likely a tall order", following conversations it had with several industry players and the financial results of the project's key contractor, Iris Corp.

"As such, there could be changes in the development and deployment of NIISe, which may: i) affect the timeline in returning of foreign workers’ work permit renewal services to the Immigration Department; and ii) present new business opportunities for industry players, including MyEG," it said.

Nevertheless, the news and policy risks are expected to weaken investors’ interest in MyEG, considering the material revenue contribution from its immigration-related businesses.

"On the other hand, MyEG’s steady 2022-24 earnings outlook, stable revenue from the road-transport businesses, exciting new business opportunities (the Road Transport Department's e-testing system, and blockchain initiatives), and potential business opportunities from NIISe-related works should help support its share price," it added.

Hence, while it maintained its earnings forecast for the stock, it lowered the valuation multiple to 19 times its estimated 2023 price-earnings ratio — from 25 times — due to heightened policy risks.

"Key upside risks to our view are favourable changes in the Immigration Department’s outsourcing policy, better-than-expected financial performance, strong pickup in its blockchain business, and securing new contracts to develop and deploy e-government services. Downside risks to our view are unfavourable changes in the government policies, lower-than-expected financial performance, and weak adoption of MyEG’s Zetrix blockchain," it added.

Read also:

MyEG: No meeting held with Putrajaya on reverting immigration services back to govt

MyEG’s Zetrix blockchain to launch mainnet on April 15

MyEG is confident in getting another three-year extension for e-govt concession

The content is a snapshot from Publisher. Refer to the original content for accurate info. Contact us for any changes.

Related Stocks

| IRIS | 0.300 |

Comments